December 2020

Stephen Evans, chief executive of Learning and Work Institute

The sharp rise in redundancies is likely to be partially due to the anticipated end of the furlough scheme before it was ultimately extended. Overall, unemployment has risen sharply this year, although measures like the furlough scheme have limited the damage.

The rollout of a vaccine gives hope for 2021. But the prospect of tighter restrictions early in the year in response to any Christmas virus surge suggests further trouble ahead. The likelihood of either no deal or a relatively thin trade deal with the EU is also likely to lead to an increase in unemployment while our analysis shows a sharp rise in long-term unemployment is already baked in for 2021.

All of that means that the Government is likely to need to go further and faster. The Restart programme is due to go live in the summer, too late for the likely surge in numbers long-term unemployed in the spring. We urgently need more help for people to find work and employers to create jobs.

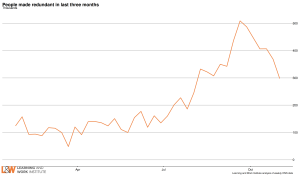

Redundancies are at their highest levels since 2010

In part, the rise in redundancies may reflect the anticipated end of the Coronavirus Job Retention Scheme at the end of October, before the scheme was ultimately extended.

The high level of redundancies is likely to be related both to the reintroduction of tighter restrictions to curb the spread of the virus, and to uncertainty for businesses generated by the anticipated end of the Coronavirus Job Retention Scheme (CJRS).

The government had been planning to withdraw the CJRS at the end of October, and replace it with the Job Support Scheme, which would have been more restrictive and less generous. As the pandemic worsened again, and measures to control the spread were re-introduced, the government announced on 31st October that the CJRS would be extended until December, before announcing on 5th November that the CJRS would be extended until the end of March 2021.

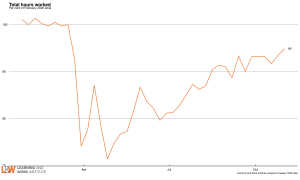

The CJRS has helped to limit the potential impact of the pandemic on employment. The latest HMRC data shows there were still 1.5m workers fully furloughed at the end of September. Today’s data from the labour force survey shows that the number of hours worked across the economy remains 5.1% down on the pre-crisis level, whereas employment has only fallen by 1.5%.

Unemployment and long term unemployment

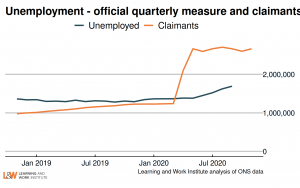

Today’s data shows that both unemployment and long-term unemployment have risen significantly since the onset of the pandemic.

Unemployment is 1,692,000, an increase of 32% since this time last year. Long term unemployment – which measures the number of people who have been unemployed for 12 months or longer – now stands at 356,000, and increase of 105,000, since the last quarter.

The rise we have already seen in long term unemployment relates not to people who lost their job as a result of the pandemic, but to people who became unemployed before the pandemic. People who were out of work as the crisis began will have found it more difficult to find work as the number of vacancies has plummeted and competition for the jobs that are available has intensified.

Recent Learning and Work Institute research warned that long term unemployment is on course to surge further next year. At last month’s spending review, the Chancellor announced the £2.9 billion Restart scheme, which aims to provide support for long term unemployed people to return to work.

Unemployed claimant levels remain very high – the rise in the international measure of unemployment remains well behind

There are still 2.7 million people unemployed and claiming benefits as unemployed as we move towards Christmas. 88% of these people, over 2.3 million are claiming Universal Credit. The remaining 330,000 are claiming Jobseeker’s Allowance.

Since last year, the claimant count has risen by 1.44 million or 117.2%.

People claiming Universal Credit have benefitted from a £20 per week increase in Universal Credit which was announced in March to protect incomes during the crisis. The increase is due to last until the end of March 2021.

With hundreds of thousands more people claiming Universal Credit, and with unemployment likely to increase further as the pandemic spreads and as the CJRS comes to an end, the Chancellor has come under growing pressure to retain the £20 increase and to give the same increase to those on older benefits such as Jobseeker’s Allowance and Employment and Support Allowance. Modelling by Joseph Rowntree Foundation suggests that the Universal Credit increase’s withdrawal could mean 500,000 more people falling into poverty, including 200,000 children.

But a Happy New Year…? The labour market prospects for 2021

There are some silver linings. The rapid development of several seemingly effective vaccines, and the beginning of the vaccine rollout, offers the opportunity to bring the pandemic under control in spring and summer of next year. This could reduce the need for social distancing requirements, allowing many sectors to bounce-back as the year progresses. The success of the furlough scheme and other measures may limit the long-term damage from this year.

However, there are dark clouds on the horizon. The Office for Budget Responsibility (OBR) expects unemployment to peak at 2.6 million next year in the April to June period even with a trade deal with the EU. Any failure to agree a post-Brexit trade deal is likely to lead to a further shock to the economy. OBR’s forecasts suggest that no deal would mean unemployment rising further, peaking at 2.8 million in July to September next year and staying higher for longer than under its central scenario. With no deal, OBR expects unemployment to stay above 2 million until the first three months of 2024 compared to a year earlier with a trade deal.