January 2022

Stephen Evans, Chief Executive at Learning and Work Institute, said:

The year ahead will be dominated by the cost of living crunch and labour shortages. Today’s data shows prices rose faster than wages in November. With higher inflation and tax rises still to come, the Government needs to help households: the cost of living crunch has only just begun.

At the same time, rising numbers of people with long-term sickness mean there are one million people fewer in the labour market than on pre-pandemic trends. We need to support more people to look for work for employers to fill record vacancy levels. We must do so in a jobs market showing some signs of slowing even before any effects of Omicron. Employment is still recovering, but on the best measure remains 600,000 down on pre-pandemic levels. The Plan for Jobs has made a real difference, but the Government should not overclaim on the basis of payroll employment figures that don’t cover everyone in work. This is still mission progressing, not mission accomplished.

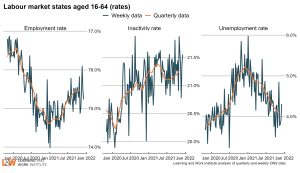

1. The labour market continues to recover, though employment remains below pre-pandemic levels

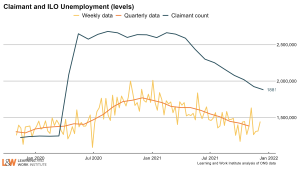

Employment rose by 60,000 in September to November 2021 compared to the previous quarter but remains 598,000 lower than before the pandemic. The timelier but less comprehensive measure of PAYE employees increased by 184,000 in December 2021 compared to the previous month and is 410,000 above its pre-pandemic level. Unemployment fell by a further 128,000, but economic inactivity has risen and is now 411,000 higher than pre-pandemic.

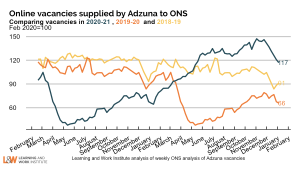

The number of vacancies in the ONS vacancy survey remains at record levels. The number of online postings supplied to Adzuna has dropped back, but this reflects usual Christmas patterns and it remains 26% above the same week in 2018.

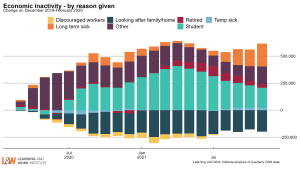

2. A lower economic activity rate means fewer potential workers for employers to recruit

Our analysis shows there are 1.1 million fewer economically active people (either employed or unemployed) than if pre-pandemic trends had continued. Around one third is the result of a lower population, two thirds due to people stopping looking for work (growth in economic inactivity).

The number of economically active people fell during the pandemic, partly due to lower vacancies, health concerns and economic restrictions. Worryingly, economic inactivity is now rising again, after falling in the second half of 2021. This helps to explain the difficulty some employers are reporting in filling vacancies – there are fewer people looking for or available for work. The 2.3 million people economically inactive due to long-term sickness or disability, up 5.5% in the last quarter, should be a key focus.

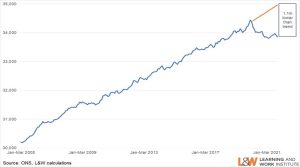

In addition, the number of people claiming unemployment-related benefits remains 498,900 above the survey measure of unemployment, despite a fall of 43,300 in December 2021 compared to the previous month. It is important that Jobcentre Plus engage with all of those on out-of-work benefits to ensure their status is recorded correctly and everyone who wants to work gets help to find a job.

3. Prices rose faster than wages in November, suggesting a cost of living crunch is already underway

The latest data show average earnings grew by 3.5% in the year to November 2021. With the Consumer Price Index rising by 5.1% in the year to November 2021, this means that real wages fell in November and are likely stagnant at best since then.

Care should be attached in interpreting average earnings data. It has been affected through the pandemic by the impact of the furlough scheme and also changes in employment (for example, lower paid workers were more likely to lose their jobs).

However, this picture is clearly some distance off the high wage future some argued was here when the initial supply chain crunch as pandemic-related restrictions were lifted led to some rises in wages for some occupations in particular.

This cost of living crunch has only just begun, with rises in National Insurance already planned for April, further rises in inflation expected, and a sharp rise in the energy price cap ahead. The Government should step in to provide help for households’ finances and to fix some of the underlying drivers of these challenges.

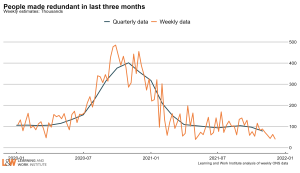

4. There are few signs of the end of the furlough scheme leading to a significant increase in unemployment

There were 1.14 million people furloughed at the scheme’s end in September 2021, of whom 640,000 were fully furloughed. The signs are that the end of the scheme has had relatively little impact on employment. The number of people made redundant was the lowest on record (since 1995).

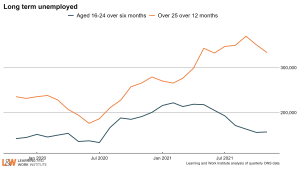

5. Long-term unemployment remains above pre-pandemic levels, but it’s good news that it’s fallen somewhat for both young people and older adults

Long-term unemployment is a particular concern as it reduces people’s chances of finding work and can reduce their health and wellbeing.

Long-term unemployment rose significantly through the pandemic. It has fallen recently for young people though is still 11,000 higher than pre-pandemic. There are 96,000 more people aged 25 and over out of work for 12 months or more than before the pandemic (Dec 19-Feb 20), though signs this may now be falling (either due to people finding work or moving into economic inactivity).

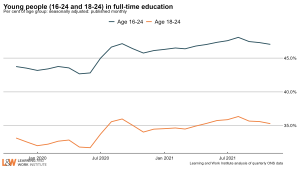

There have been rises in the number of young people staying in full-time education through the pandemic. This can be a sensible response to a tough labour market and, if the education is high quality, helps tackle some of our skills shortfalls with other countries. Overall, though, support for young people remains too disjointed: we argue for a Youth Guarantee to offer all 16-24 year olds a job, training place or apprenticeship.