Every month, Learning and Work Institute produces detailed and timely analysis of the latest labour market statistics from ONS. We examine what the figures tell us both about the health of our labour market, and what they mean for people’s experiences of work, with a particular focus on groups facing labour market disadvantage. Become a supporter to receive our monthly briefing delivered directly to your inbox and navigate our labour market dashboard.

January 2026

Stephen Evans, chief executive of Learning and Work Institute, said:

The labour market remains flat with the number of payroll employees estimated to have fallen again. Underneath this headline picture are further worrying falls in payroll employment in retail and hospitality, down 142,000 in a year. This contrasts with rises of 52,000 in health and social care and public administration. Looking ahead, slow growth and global instability increase the risks of rising worklessness, increasing the importance of the Government focusing on growth.

There are no major changes this month, but the signs of an easing labour market remain

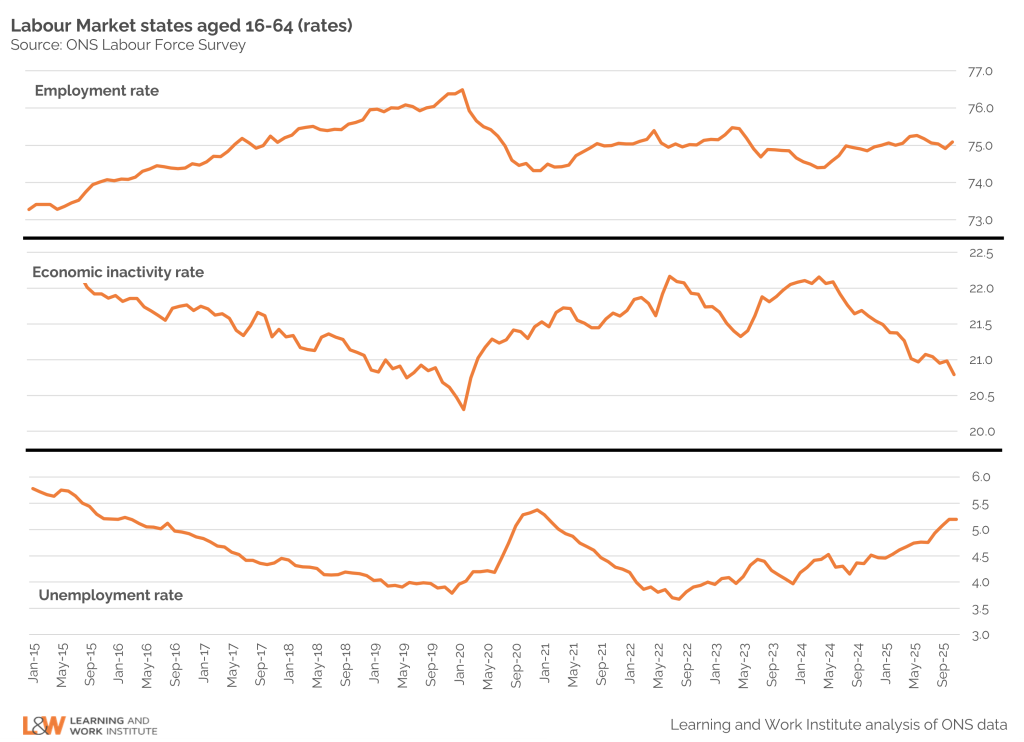

There are no major changes in the latest labour market figures, but there are plenty of signs pointing to a gently easing labour market. In the most recent figures (Sept-Nov 2025) unemployment is at 5.2% – 0.7 ppt higher than a year previously, and the highest level since 2021. Employment is now at 75.1% and economic inactivity (people who are out of work and not currently trying to get into work) appears to be continuing its downward trajectory and is now at 20.8% (compared with 21 .6% in the same period a year ago).

We are continuing to treat those trend numbers with some caution, given the well-documented post-pandemic issues with the Labour Force Survey. Payroll employment – the number of people employed in jobs (so excluding self-employed people) fell by 43,000 between November and December 2025, and is 184,000 lower than the same time last year. These are not catastrophic changes, but show that widely reported anecdotes of a challenging jobs market are reflective of the underlying reality.

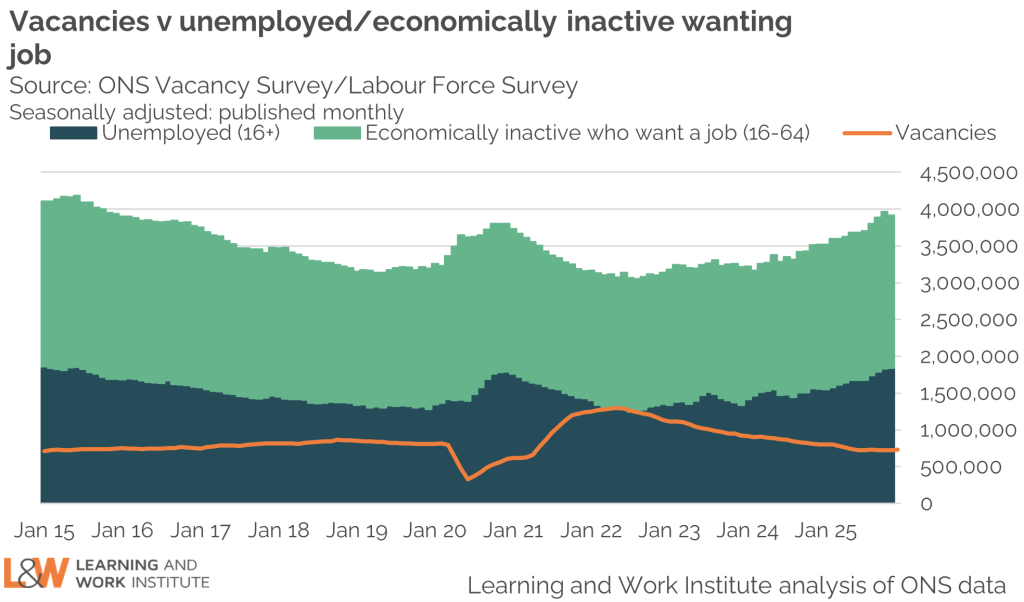

For every vacancy, there are 5.4 people who want a job – 1.5 more than pre-pandemic

This chart shows the problem: the number of vacancies have been going down, while the number of people out of work (who want to be in work) has been going up.

The latest provisional data from Oct-Dec 2025 suggests that the number of vacancies may be starting to rise following the long decline from a post-pandemic peak (up to around 730,000 after hitting a low of 722,000 last summer).

But there are still around 5.4 people wanting work for every vacancy – 1.8 million unemployed people, and a further 2.1 million people who are economically inactive but say they want a job.

This is high – although still well below the post-crash peak of the early 2010s when that ratio reached 11 seekers for every vacancy. So we have an easing labour market right now – but nowhere near recession levels.

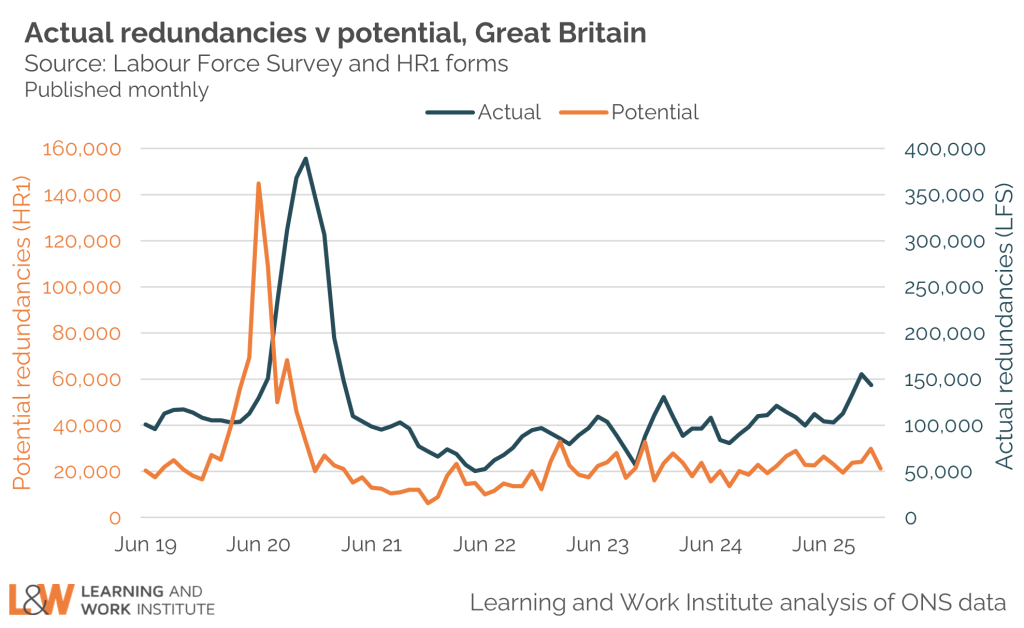

Meanwhile, redundancy levels remain substantially higher than they were this time last year – 145,000 in the most recent quarter (Sept-Nov 2025), up from 112,000 the year before.

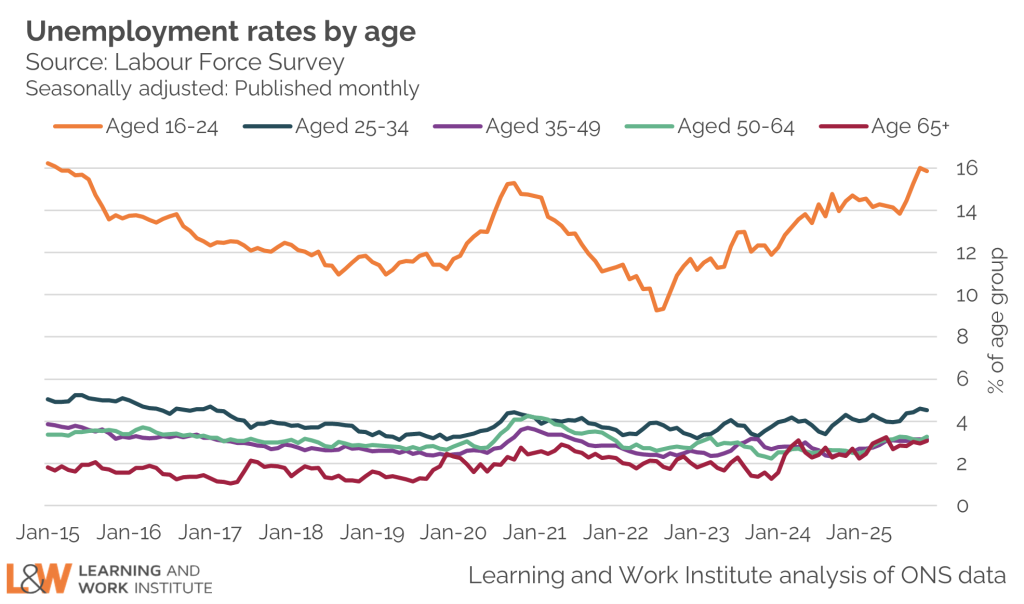

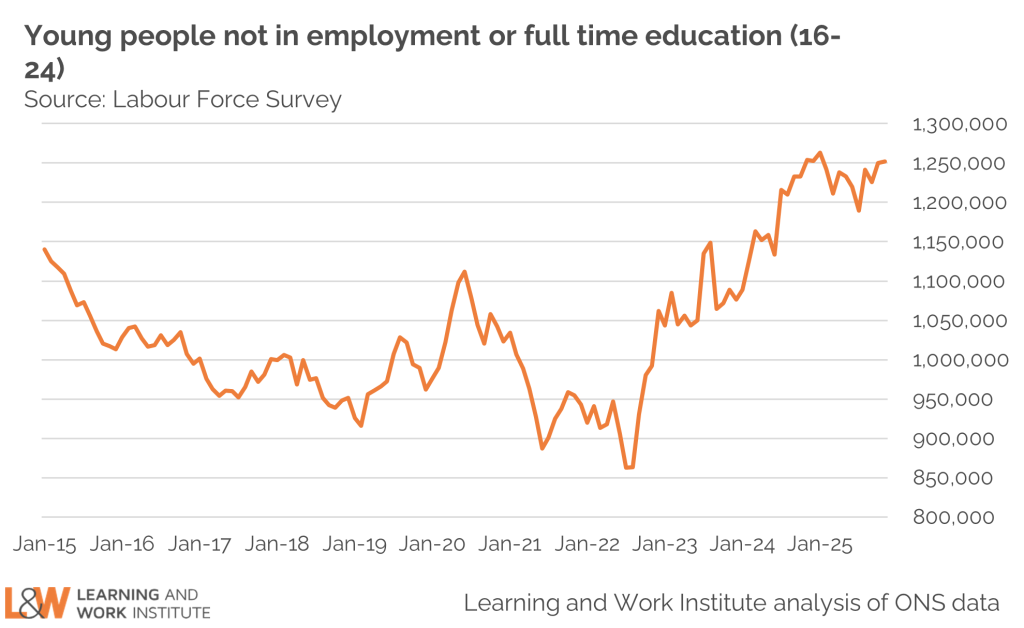

Youth employment remains the big story – with unemployment rates for young people at 15.9%

There is no doubt that young people – a generation who have had their education and entry to the jobs market marred by the pandemic – are facing a challenging jobs market, and their struggles remain the big story in the labour market data.

The overall unemployment rate (for 16-64s) has risen by 0.7 ppts since Sep-Nov 2024. But among young people (age 16 to 24) – it has risen by 1.4 ppts, and now stands at nearly 16%. NEET levels – the number of young people who are in neither employment, full-time education or training – are no longer consistently rising, but there are still 1.25 million 16-24s in that group, only just below the January 2025 peak.

This cohort continues to be the major focus for policymakers both nationally and around the country in strategic and local authorities. Youth Guarantee ‘trailblazers’ are now rolling out in many parts of the country, with strategic authorities attempting to join up services and engage more young people in the opportunities in their area. The Government announced a substantial package of DWP-funded measures for Universal Credit claimants at last autumn’s budget – including subsidised work placements for young people who had been out of work for a long time, and additional job coaching prior to that point. Those measures are targeted at stemming the tide of rising long-term unemployment among young people.

The latest announcement is an attempt to get a handle on the root causes of rising youth worklessness: an ‘investigation’ by former Health Secretary Alan Milburn. This is currently seeking evidence and will report later this year.

Job numbers are falling in retail and hospitality – but also construction and manufacturing

One of the challenges facing young people is the contraction of the labour market in industries where many of us traditionally have taken our first steps into the world of work.

Data from HMRC PAYE data – which tells us how many ‘jobs’ there are in different parts of the economy – shows that jobs are down in both retail and hospitality. There are 72,000 fewer jobs in retail than there were this time last year, and 70,000 fewer jobs in hospitality. The increases are in the public and health sectors: there are 37,000 more jobs in health and social work and 16,0500 in public administration and defence.

On social media sites and message boards across the internet, AI is named by jobseekers as the major culprit in this challenging jobs market. This is a rapidly changing picture with only very tentative (and conflicting) research evidence available – but there are no clear signs of AI impact in this high-level data. According to the PAYE data, the biggest fall in jobs (78,600) has been in the category “administrative and support services”, but this describes a type of employer – such as security services, call centres and travel agents – rather than a type of job. AI might be part of the picture here – but so too is offshoring, and a broader contraction of less productive business struggling to absorb rising costs.

It is worth noting that construction and manufacturing – two of the priority sectors for skills growth identified by Skills England – have also seen a fall in jobs over the last year, although the changes are not large.

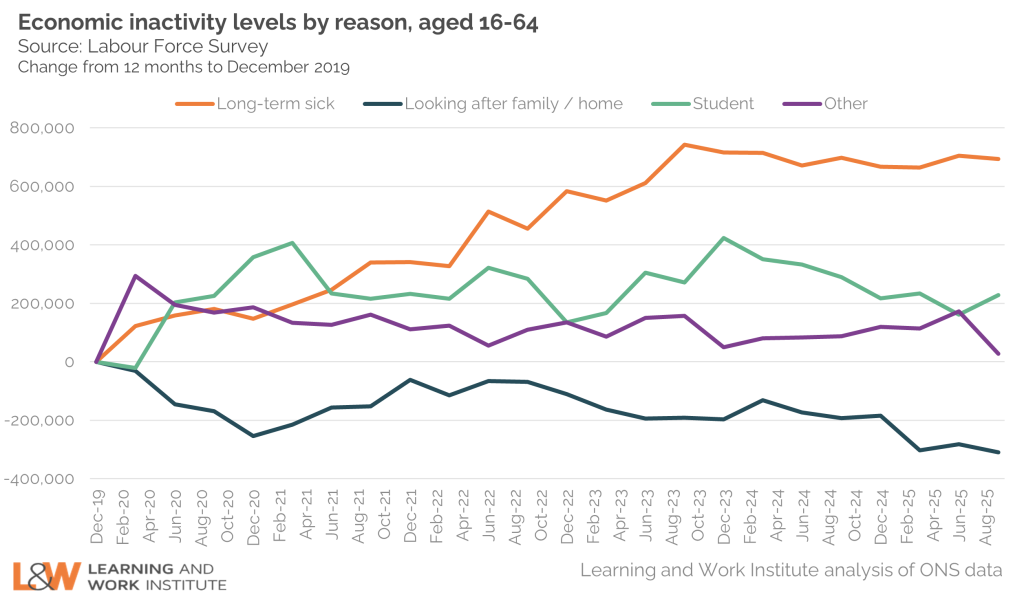

The impact of health on work remains a major concern

The impact of ill-health on labour market activity remains a major concern for the Government. The number of people who are out of work due to their health is substantially higher now (2.8 million in September-November 2025) than it was pre-pandemic (2.1 million in December-February 2019).

The Labour Force Survey data suggest that this is a problem which is bad, but not worsening – levels have remained broadly flat over the last two years. But this will not be giving much solace to the Government.

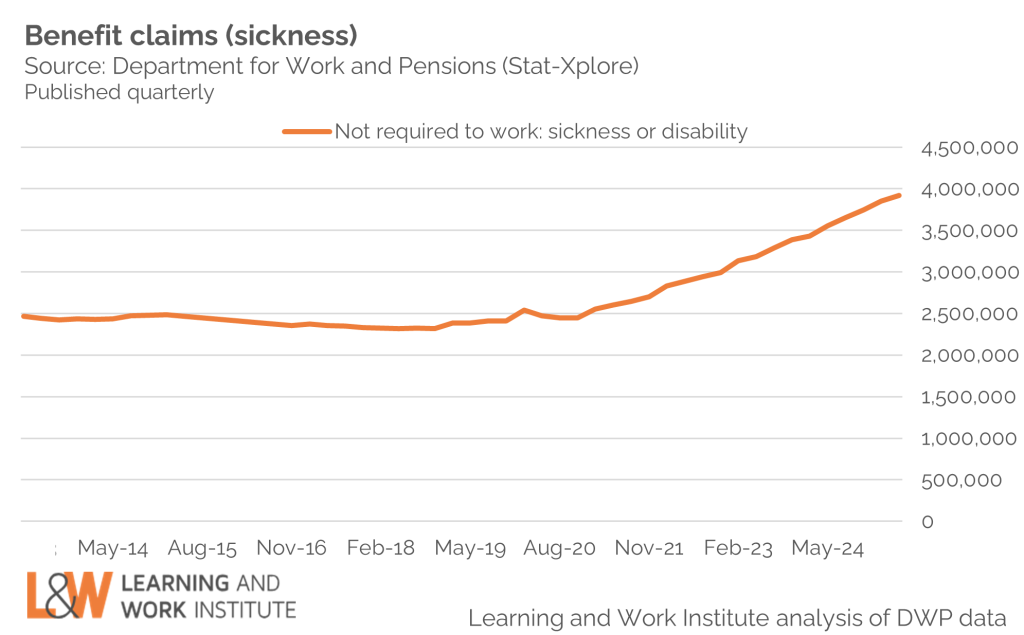

That’s because the number of people on Universal Credit (and other benefits) who have been judged not fit for work due to ill-health has continued to rise over this period – now standing at around 3.9 million. That’s the number that DWP will be the most focussed on – as it makes the most immediate difference to the public purse. This is a subset of the group of people who are economically inactive due to their health; of a group of people whose financial situation means they can and need to access Universal Credit, and whose income is directly tied to their health status.

The Government’s approach to this group has fundamentally shifted course since their attempt to reform disability benefits – and save money – failed last year following major opposition from their own MPs. The intent to reform personal independence payments and increase the disability employment rate remains, but cost savings are no longer front-and-centre and ‘support’ has got higher billing. Since the December labour market statistics release, the DWP Minister for Disability Stephen Timms has announced a higher threshold of activity for employers to participate in the (voluntary) ‘disability confident’ scheme – and just today DWP announced an expansion of their health-focussed employment scheme ‘WorkWell’.

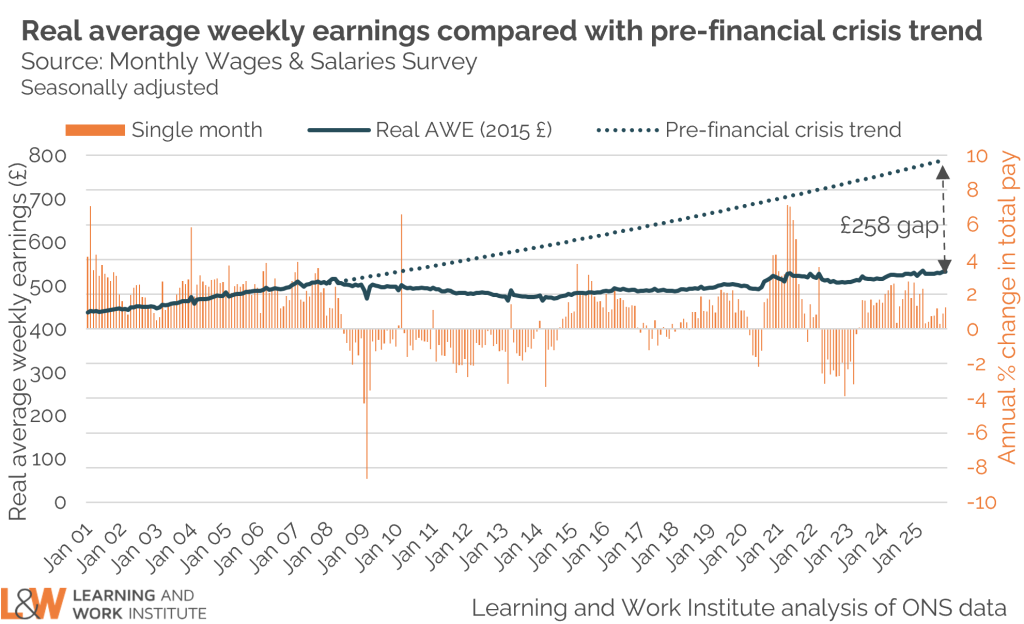

Pay growth remains both too weak and too strong…

Long-term pay growth has been weak: we are on average £258 worse off per week than we would be if pre-financial crisis trends had continued. That is an immediate challenge to the pockets of people across the country who are struggling to meet the cost of living.

But at the same time, the rate of pay growth is presenting challenges to the economy in the opposite direction. Given the OBR’s projection of a 1% productivity growth trend in the coming years, we will only keep inflation at 2% in the medium-term if nominal wage growth is limited to around 3%. But right now, wage growth is at 3.6% in the private sector, and 7.9% in the public sector (though this is affected by the timing of previous years’ settlements) – a situation which puts us at risk of persistently high inflation, not rising living standards. If we want sustainable wage growth, then we need to see faster productivity improvements – and a more dynamic, skilled, and accessible economy and workforce.

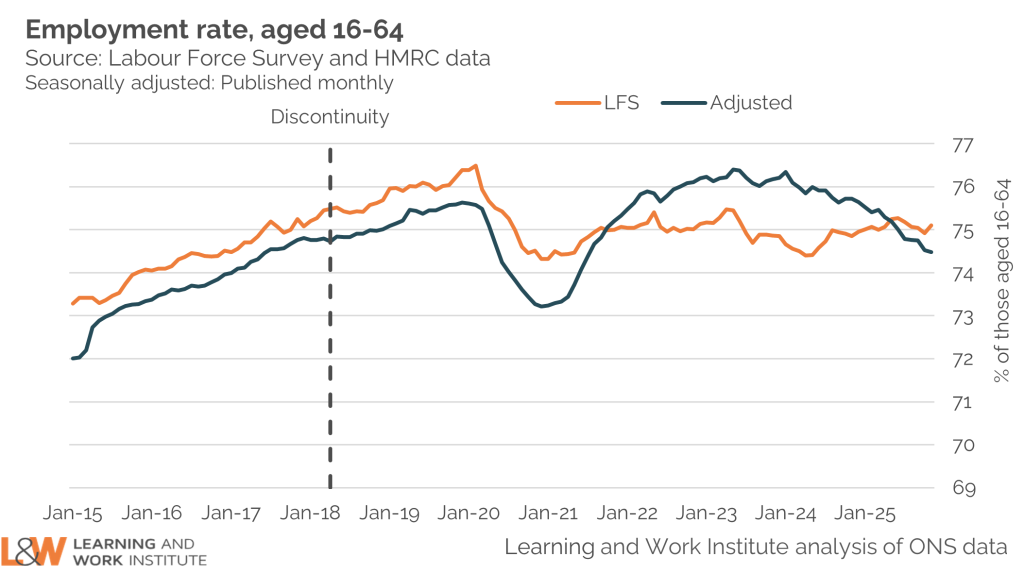

Can we trust this data?

Our headline indicators are based on data from the Labour Force Survey, but since the pandemic this has experienced a decline in the response rate which affects the reliability of estimates from this source. This is illustrated by the divergence in the employment rate estimated from the LFS and other sources over this period. While the ONS seeks to resolve these issues, we are publishing an experimental estimate of the employment rate based on an approach developed by the Resolution Foundation and using administrative data sources, such as HM Revenue and Customs payroll and self-assessment data on the numbers of people self-employed.

The divergence is substantially less stark than it was – suggesting that the LFS is becoming more accurate. However, while the short-term trends may now be starting to align in the two data sources, the adjusted data series points to a much sharper decline in employment rates over the last year (from a higher starting point) – further evidence of a cooling labour market, and confirmation of the headache this Government faces.