Every month, Learning and Work Institute produces detailed and timely analysis of the latest labour market statistics from ONS. We examine what the figures tell us both about the health of our labour market, and what they mean for people’s experiences of work, with a particular focus on groups facing labour market disadvantage. Become a supporter to receive our monthly briefing delivered directly to your inbox and navigate our labour market dashboard.

March 2026

Stephen Evans, chief executive of Learning and Work Institute, said:

Worryingly, the number of young people not in employment or full-time education remains stubbornly stuck at 1.25 million. Recent announcements including hiring incentives for employers will help, but mostly miss the three in four NEETs not on unemployment-related benefits. Overall the labour market remains pretty flat, with little change in the main measures of employment and vacancies and earnings growth continuing to ease. That leaves the Government needing another two million people in work to hit its 80% employment rate ambition. With economic risks ahead there’s much more to do.

Young people facing the biggest challenges in a stagnant labour market

Unemployment among the 16-24s has reached 16% – the highest rate in over a decade – and youth employment (or lack thereof) is once again the big story this week. This follows a slew of toothy announcements from DWP Secretary of State Pat MacFadden on Monday. The Government has expanded its ‘Jobs Guarantee’ scheme – giving fully subsidised 6-month work placements to young UC claimants seeking work for 18 months – from 18-21 to 18-24s, and announced an additional financial incentive for employers hiring from that group before they hit the 18-month mark.

Today’s numbers remind us why the Government felt moved to offer financial incentives: the jobs market is still looking sluggish, with plenty of jobseekers out there seeking work. There are 5.4 people wanting to work for every vacancy, and wage growth in the last quarter was the lowest it has been since the height of the pandemic. Employers are facing a range of challenges which might slow their hiring decisions, from rising National Living Wage rates (although there are reports that increases to young people’s NLW are being paused) to what we might euphemistically describe as “global geopolitical and economic uncertainty”.

In this context, it makes sense for Government to try to put their thumb on the scales for NEET young people, and offer employers further incentives to take a leap and recruit. We reckon the subsidy measures announced this week could support around 180,000 jobs in total.

These investments are not insignificant, but by themselves they won’t be enough to tackle the problem at large. Only around a quarter of NEET young people are in that UC Searching for Work group that these programmes are targeted at. The next step is for Government to join up and extent the ‘Trailblazer’ programme of experimental local support into a comprehensive offer to the other 3 in 4 NEETs.

Earlier this week, the Big Boss (AKA our Chief Exec Stephen Evans) set out why this matters, what it means, and where we need to go next. Today, your humble Director of Research and Policy offers some charts to chew over, to help put those announcements into context.

Do you have suggestions for how we can make this briefing better, or more useful? Your author is keen for feedback – email Emily.Andrews@learningandwork.org.uk if you have specific asks/pointers on what you want to see for us?

The context

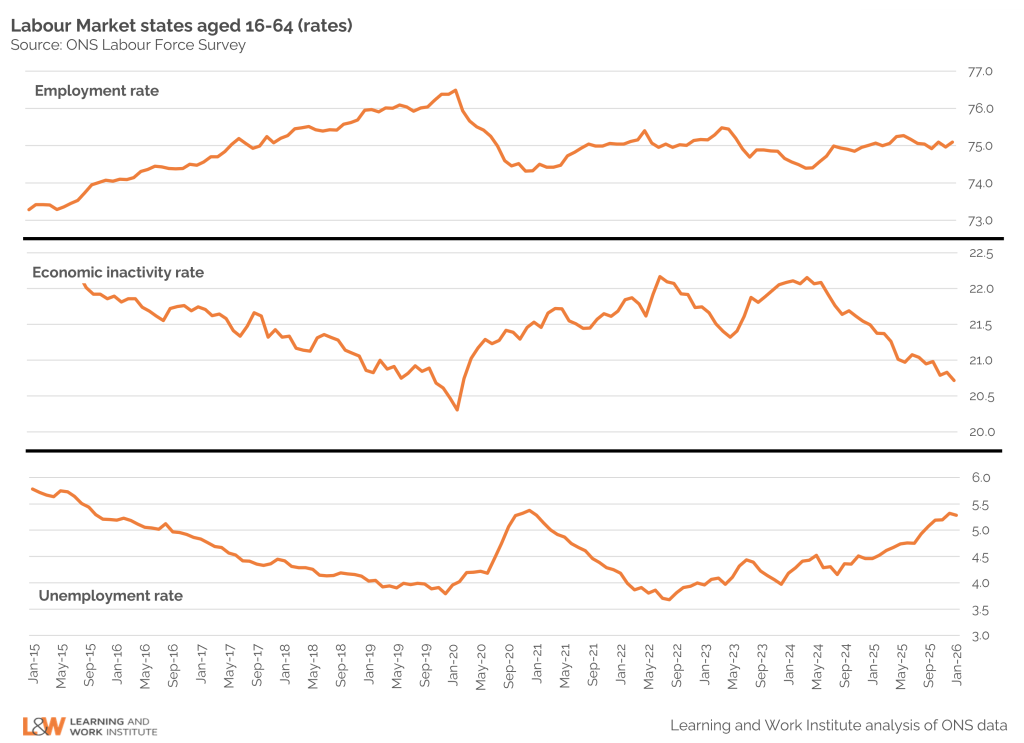

No big changes in the headline employment stats: unemployment is at 5.3%

The headline figures for the latest quarter – which cover the three months up to January this year – show a flat labour market. The employment rate continues to hover around 75% as it has done since late 2024 (75.1% in the latest figures). Unemployment continues at its recently somewhat elevated level (5.3%), but is only up 0.1ppts on the previous quarter.

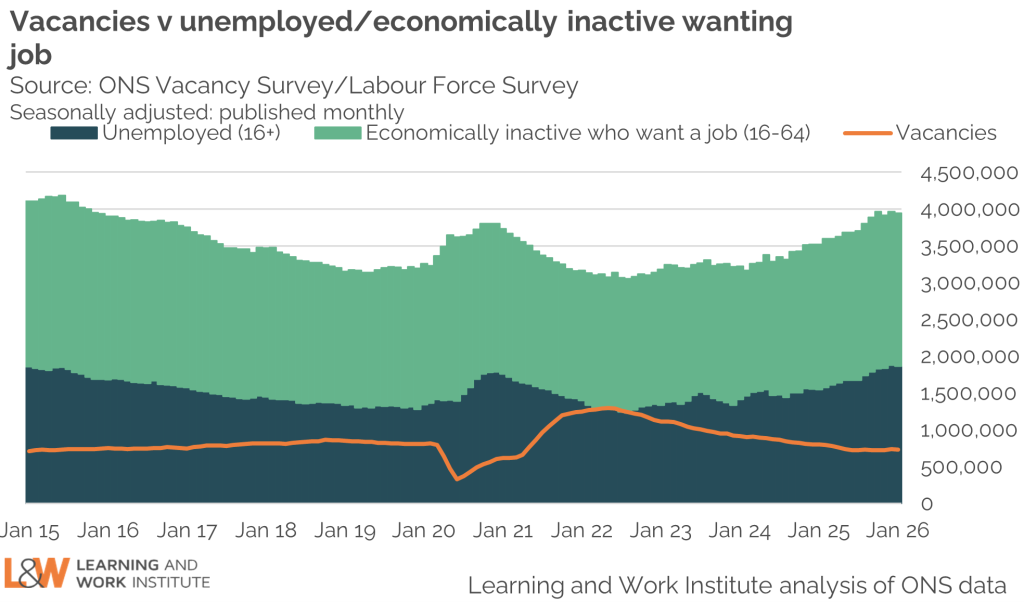

There are 5.4 out-of-work people looking for a job for each vacancy: 1 more than a year ago

There are currently 5.4 people who are out of work and want a job for every vacancy, compared with 4.4 a year ago. All the numbers have moved in the wrong direction: there are both fewer vacancies (730,000 compared with 799,000) and more jobseekers than there were 12 months ago. As with the headline employment stats, not much has changed in the last quarter – but the overall picture is of a stuck labour market.

The youth challenge

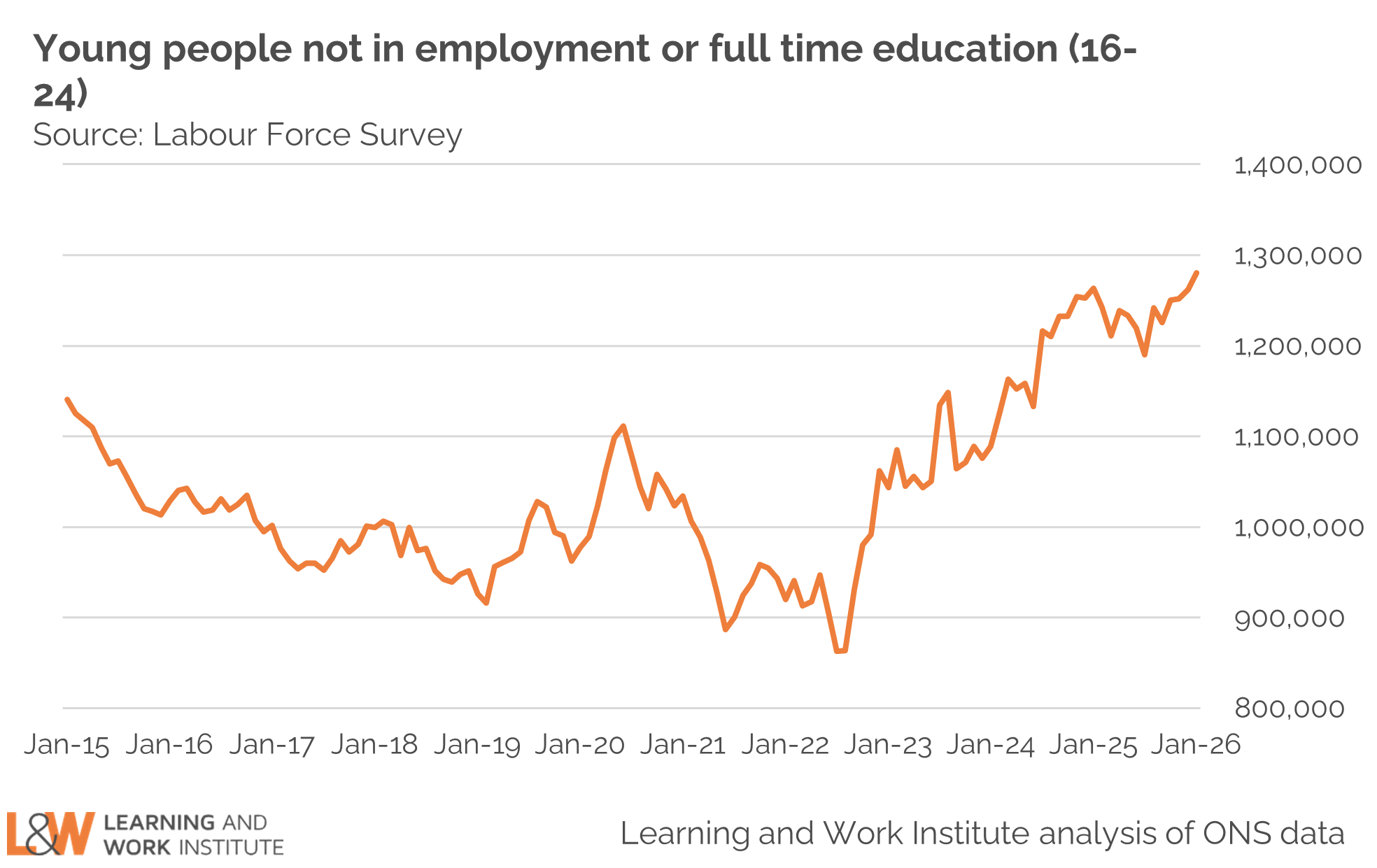

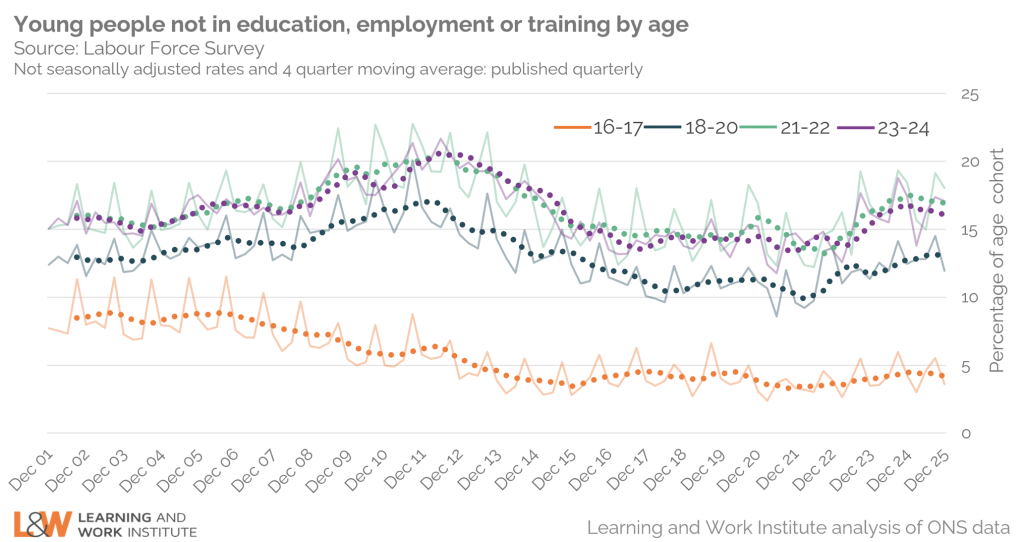

There are still 1.28 million young people not in employment or full-time education.

The number of NEET young people is continuing to tick upwards: there are currently 1.28 million 16-24s not in employment or full-time education. The numbers of young people overall is also growing, so while numbers NEET have climbed over the last couple of years, the rates have stayed broadly flat – 19.2% for 18-24s (the same as a year ago) and 9.4% for 16-17s (down from 9.6% a year ago) – following major post-pandemic increases.

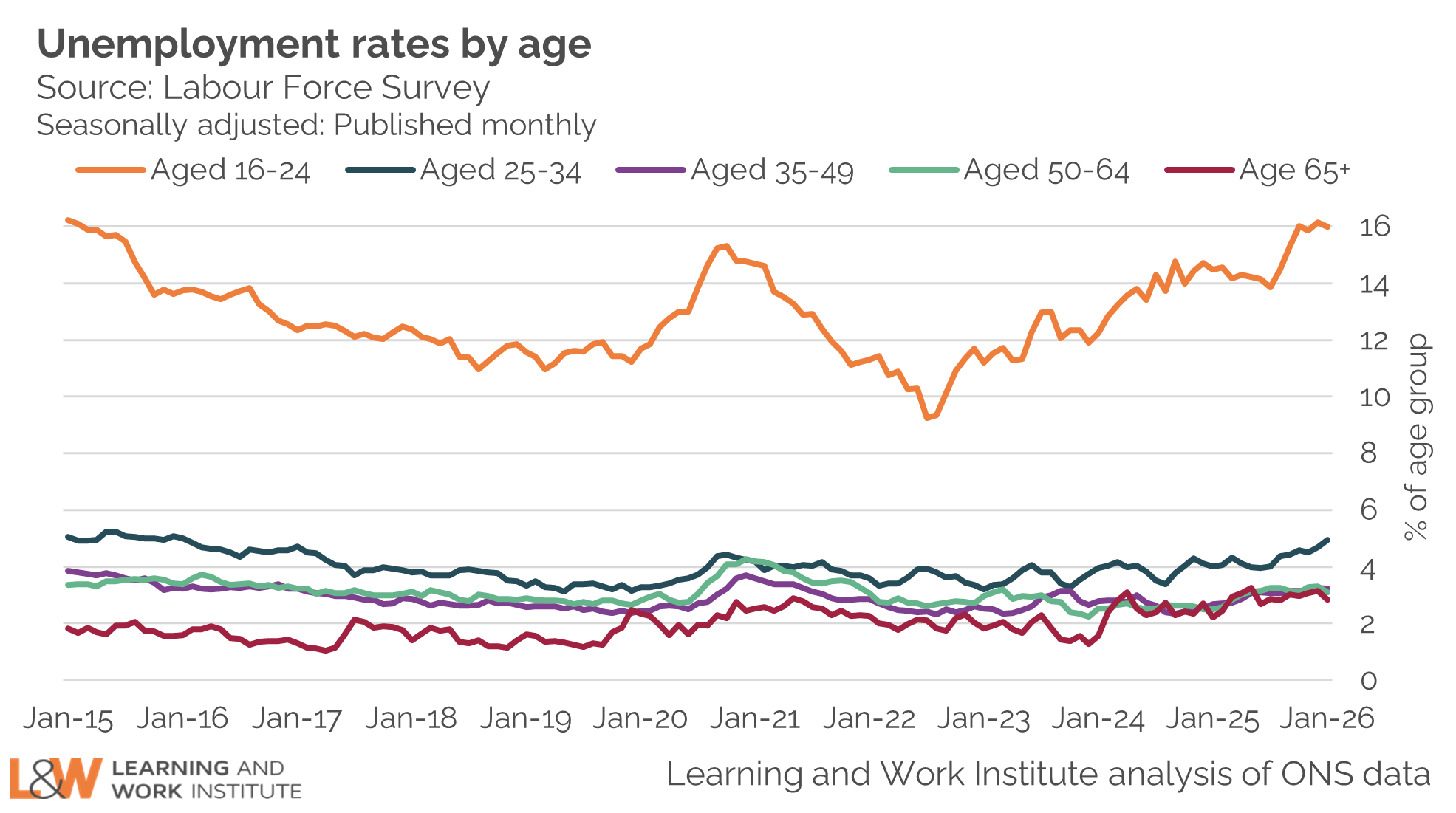

The unemployment rate for 16-24s has climbed much faster than older groups

Comparing unemployment rates between different age groups highlights just how stark the youth challenge is. Since 2022, unemployment among 16-24s has risen by 6.7 ppts (from 9.2% in July 2022 to 16% in the latest data), while it has risen by less than 1 ppt among 25-64s over the same period.

21-24s are the group most likely to be NEET

The NEET issue is most pronounced at the older end of the age range: detailed stats published earlier this month show that NEET rates (including young people not in any form of training at all) are highest among the over 21s. Originally, this group was excluded from many of the Government’s Youth Guarantee initiatives – but eligibility has been expanded, and on Monday the Jobs Guarantee scheme – providing subsidised 6-month placements for long-term unemployed young people – was extended up to the age of 24.

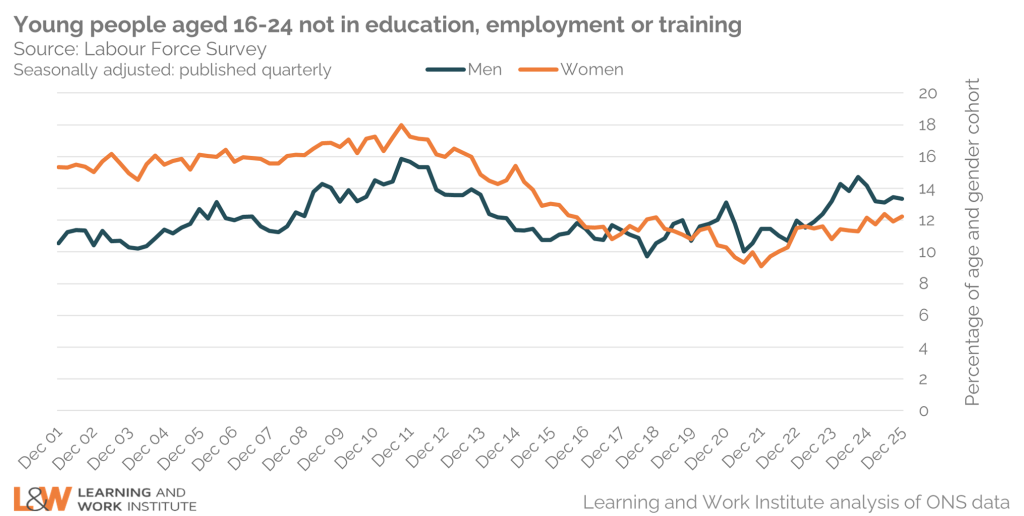

Young women are no longer more likely to be NEET than young men

Historically, young women were more likely to be NEET than young men – but the genders have converged over the last decade. Following a sharp climb in NEET rates among young men, the rates for men and women are now fairly close again (13.3% for men, 12.2% for women) but this is a trend worth keeping an eye on.

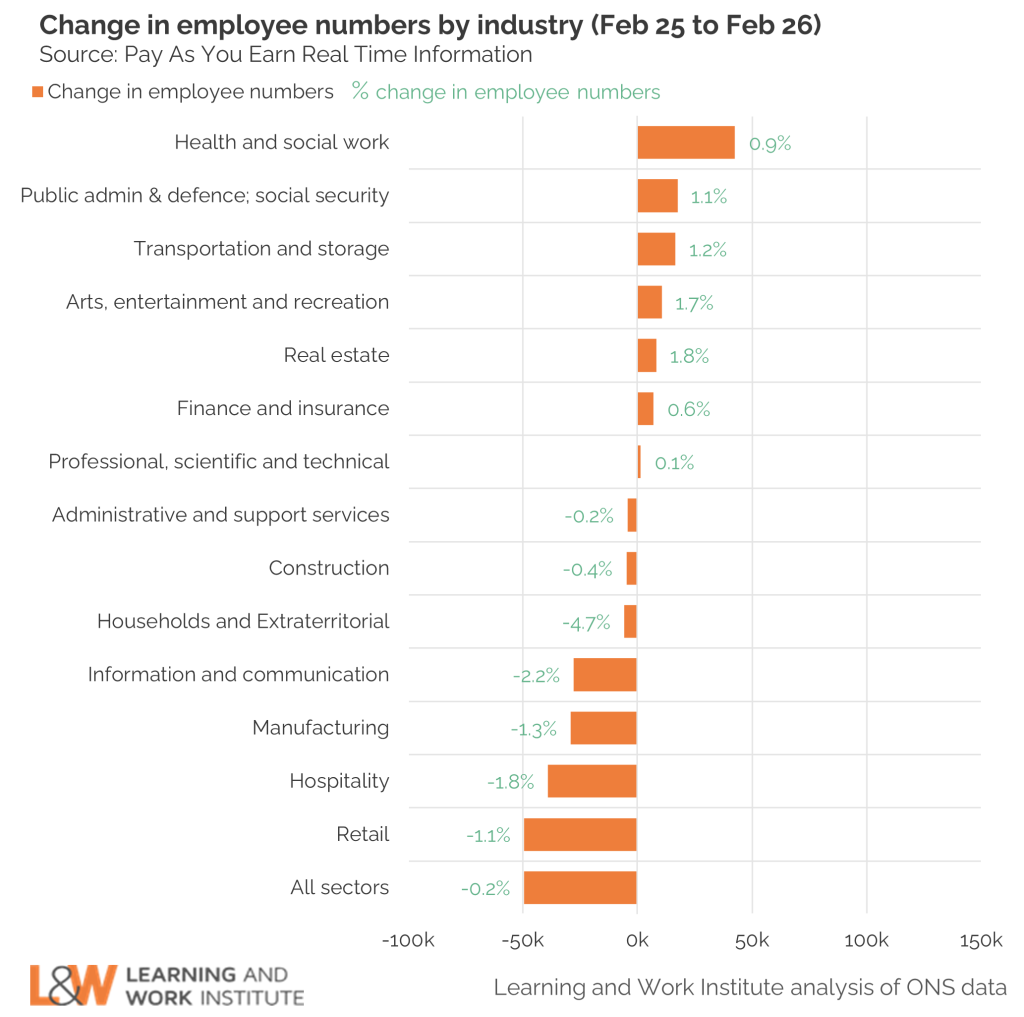

There are 88,000 fewer workers in retail and hospitality than there were a year ago

I was on the radio earlier this week, responding to whether or not we should ‘feel sorry’ for unemployed young people. The caller before me advised young people to go out and get a job in a shop or a café to get their foot in the door – but today’s stats remind us just how challenging that might be.

The number of people employed in hospitality and retail is down 1.4% overall on this time a year ago – so those tried and tested pathways into the world of work are not necessarily available. That’s why the Government’s attempts to create new opportunities for young people through work experience placements and subsidies is the right approach – giving employers an extra incentive to take a leap and provide some experience. But right now, these initiatives are still too limited, and we will need to go further to reach the 3 in 4 NEET young people who remain outside the established benefit-related systems of support.

The pay challenge

Slow wage growth presents a further sign of a cooling labour market

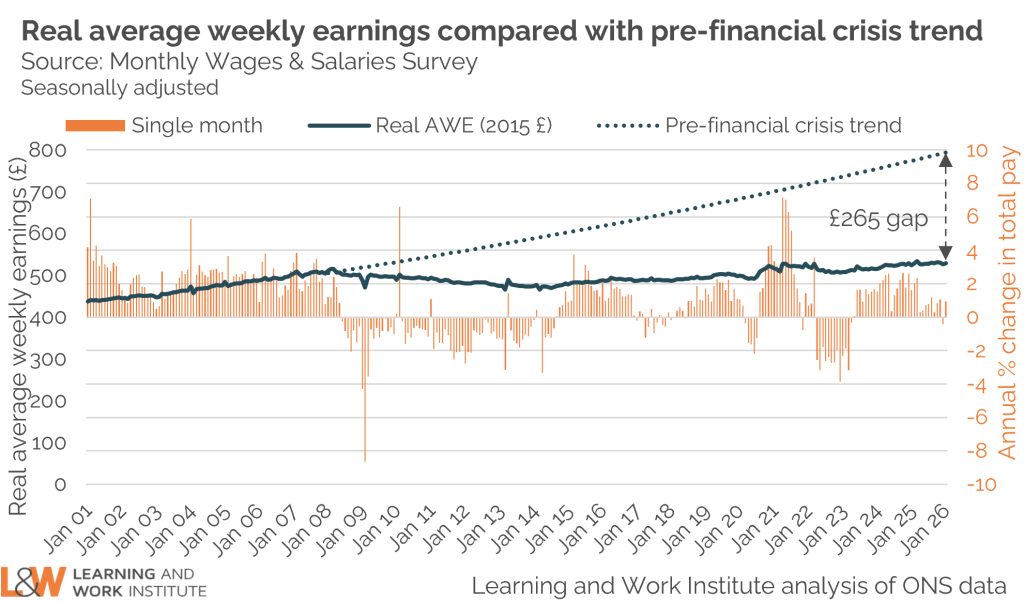

Overall pay growth was down to 3.8% in the last quarter – the lowest since the height of the pandemic. Public sector wages have seen much stronger wage growth (thanks to the timing of some previously agreed pay increases), but in the private sector wages only grew by 3.3% between November and January. On its own this might have supported the Bank of England cutting interest rates, but they now need to assess whether the recent spike in energy prices is likely to lead to a sustained increased in inflation or just a temporary blip.

For our purposes, what matters most in these numbers is that individuals have an average of £265 less in their pocket every week than pre-financial crisis trends might have given us. And employers being unable – or unwilling – to increase pay for their people are unlikely to start a hiring blitz any time soon.

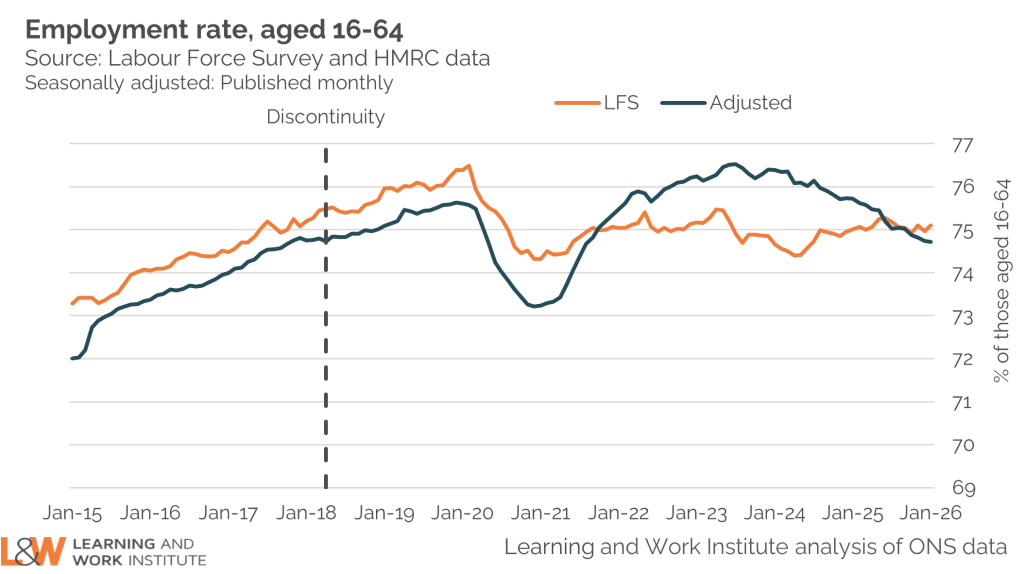

The data challenge

Our headline indicators are based on data from the Labour Force Survey, but since the pandemic this has experienced a decline in the response rate which affects the reliability of estimates from this source. This is illustrated by the divergence in the employment rate estimated from the LFS and other sources over this period. While the ONS seeks to resolve these issues, we are publishing an experimental estimate of the employment rate based on an approach developed by the Resolution Foundation and using administrative data sources, such as HM Revenue and Customs payroll and self-assessment data on the numbers of people self-employed.

The divergence is substantially less stark than it was. However, while the short-term trends may now be starting to align in the two data sources, the adjusted data series points to a much sharper decline in employment rates over the last year (from a higher starting point) – further evidence of a cooling labour market, and confirmation of the headache this Government faces.